Financial Management - Solutions

CBSE Class 12 Business Studies

NCERT Solutions

Chapter 09

Financial Management

Multiple Choice:

1. The cheapest source of finance is

(a) debenture

(b) equity share capital

(c) preference share

(d) retained earning

Ans: (d) The cheapest source of finance is retained earnings. Retained income refers to that portion of net income or profits of an organisation that it retains after paying off dividends. An organisation can reinvest its retained earnings or profits for the purpose expansion, modernisation, etc. It neither involves any fund raising cost nor any risk. Also, unlike other sources of finance it does not involve any obligation in terms of repayment.

2. A decision to acquire a new and modern plant to upgrade an old one is a

(a) financing decision

(b) working capital decision

(c) investment decision

(d) None of the above

Ans: (c) The decision to acquire a new and modern plant to upgrade an old one is an Investment decision. Investment decision refers to the decision regarding where the funds are to be invested so as to earn the highest possible return. The decision to acquire a new plant is a long term investment decision and affects long run working and earning capacity of the business.

On the other hand, working capital decisions refer to those investment decisions that influence the day to day working of the business. While, financing decision refers to the decisions regarding the sources from where the funds can be raised.

3. Other things remaining the same, an increase in the tax rate on corporate profit will

(a) make the debt relatively cheaper

(b) make the debt relatively the dearer

(c) have no impact on the cost of debt

(d) we can't say

Ans: (a) When there is an increase in the tax on corporate profit, the debt becomes relatively cheaper. This is because interest that is to be paid to the debtors is deducted from the total income before calculating the value of tax. Thus, as the value of tax increases, the debt becomes relatively cheaper.

4. Companies with a higher growth potential are likely to

(a) pay lower dividends

(b) pay higher dividends

(c) dividends are not affected

(d) none of the above

Ans (a) Companies which have higher growth potential are likely to pay lower dividends. This is because the companies having higher growth potential have greater investment plans and require larger funds for investment. Thus, they retain a greater portion of their earnings to finance the required investment and thereby, pay lower dividends.

5. Financial leverage is called favourable if

(a) Return on investment is lower than the cost of debt

(b) ROI is higher than the cost of debt

(c) Debt is easily available

(d) If the degree of existing financial leverage is low

Ans: (b) Financial Leverage refers to the proportion of debt in the overall capital. It is said to be a favourable situation when the return on investment becomes higher than the cost of debt. In other words, as the Return on investment becomes greater, the earning per share also increases and the financial leverage is said to be favourable.

6. Higher debt-equity ratio results in

(a) lower financial risk

(b) higher degree of operating risk

(c) higher degree of financial risk

(d) higher EPS

Ans: (c) Higher debt- equity ratio refers to a situation where the proportion of debt in total capital is higher. This implies higher degree of financial risk. This is because in case of debt, it is obligatory for a business to make interest payments and the return of principal to the debtors. Thus, higher debt increases the financial risk for the business.

7. Higher working capital usually results in

(a) higher current ratio, higher risk and higher profits

(b) lower current ratio, higher risk and profits

(c) higher equity, lower risk and lower profits

(d) lower equity, lower risk and higher profits

Ans: (a) Working capital of a firm refers to the amount of current assets which are in excess over current liabilities. If a company has a higher working capital then there will be a higher current ratio (i.e. current assets over current liabilities), higher risk and higher profits.

8. Current assets are those assets which get converted into cash

(a) within six months

(b) within one year

(c) between one year and three years

(d) between three and five years

Ans: (b) Current assets are those assets which can be converted into cash or can be used to pay off liabilities within a time span of 12 months, i.e. one year. Some of the examples of current assets are cash, cash equivalents, inventories, debtors, bills receivables, etc.

9. Financial planning arrives at

(a) minimising the external borrowing by resorting to equity issues

(b) entering that the firm always have significantly more fund than required so that there is no paucity of funds

(c) ensuring that the firm faces neither a shortage nor a glut of unusable funds

(d) doing only what is possible with the funds that the firms has at its disposal

Ans: (c) Financial Planning aims at ensuring that the firm faces neither a shortage nor a glut (excess) of unusable funds. If there is a shortage of funds then the firm will not be able to carry out its planned activities and commitments. On the other hand, if there are excess funds available then it adds to the cost of business and also encourages wastage of funds. Thus, financial planning focuses on ensuring the availability of just enough funds at the right time.

10. Higher dividend per share is associated with

(a) high earnings, high cash flows, unstable earnings and higher growth opportunities

(b) high earnings, high cash flows, stable earnings and high growth opportunities

(c) high earnings, high cash flows, stable earnings and lower growth opportunities

(d) high earnings, low cash flows, stable earnings and lower growth opportunities

Ans: (d) If a company gives higher dividend per share then it gets associated with high amount of earnings as only if they will earn higher, they will be able to give higher dividends; higher cash flow as the payment of dividend involves cash outflow; stable earnings as stable earnings means that the company is confident of its future earning potentials; and lower growth opportunities because it requires less requirement of retained earnings and their retained earnings while lowering the amount of dividends paid.

11. A fixed asset should be financed through

(a) a long term liability

(b) a short term liability

(c) a mix of long and short term liabilities

Ans : (a) Fixed assets are those assets which are invested in a company for a longer time period, generally more than one year. As these assets have long term implication on the business in terms of growth and profitability, they should be financed through long term liabilities such as long term loans, preference shares, retained earnings, etc.

12. Current assets of a business firm should be financed through

(a) current liability only

(b) long-term liability only

(c) both types (i.e. Long and short liabilities)

Ans: (c) Current assets are those assets which get converted in cash or cash equivalents within a short span of time and provide liquidity to a business. For financing the current assets of a business, both types of liabilities (short and long) can be used.

Short Answer Type:

1. What is meant by capital structure?

Ans:

Capital Structure means the proportion of debt and equity used for financing the operations of business.

In other words, capital structure represents the proportion of debt capital and equity capital in the capital structure. What kind of capital structure is best for a firm is very difficult to define. The capital structure should be such which increase the value of equity share or maximizes the wealth of equity shareholders.

Algebraically,

Capital Structure is

Or,

2. Discuss the two objective of Financial Planning.

Ans: Financial Planning involves designing the blueprint of the financial operations of a firm. It ensures that just the right amount of funds are available for the organisational operations at the right time. Thereby, it ensures smooth functioning. Taking into consideration the growth and performance, through financial planning, firms tend to forecast what amount of fund would be required at what time. The following are the two highlighted objectives of financial planning.

To ensure availability of funds whenever these are required: The main objective of financial planning is that sufficient fund should be available in the company for different purposes such as for purchase of long term assets, to meet day to day expenses etc. It ensures timely availability of finance. Along with availability financial planning also tries to specify the sources of finance.

To see that firm does not raise resources unnecessarily: Excess funding is as bad as inadequate or shortage of funds. If there is surplus money, financial planning must invest it in the best possible manner as keeping financial resources idle is a great loss for an organization.

3. What is financial risk? Why does it arise?

Ans: Financial risk refers to a situation when a company is not able to meet its fixed financial charges such as interest payment, preference dividend and repayment obligations. In other words, it refers to the probability that the company would not be able to meet its fixed financial obligations. It arises when the proportion of debt in the capital structure increases. This is because it is obligatory for the company to pay the interest charges on debt along with the principle amount. Thus, higher the debt, higher will be its payment obligations and thereby higher would be the chances of default on payment. Hence, higher use of debt leads to higher financial risk for the company.

4. Define a 'current asset'. Give four examples of such assets.

Ans: Current asset are those assets which are retained in the business with the purpose to convert them into cash within a short period say, one year. for example- goods are purchased with a purpose to resell and earn profit, debtors exist convert them into cash, i.e., receive the amount from them, bills receivable exist again for receiving cash against it.

Some of the examples of current assets are short term investment, debtors, stocks and cash equivalents.

5. Financial management is based on three broad financial decisions. What are these?

Ans: Financial management refers to the efficient acquisition, allocation and usage of funds of the company. It deals in three main dimensions of financial decisions namely, Investment decisions, Financial decisions and Dividend decisions.

- Investment decisions includes investment in fixed assets (called as capital budgeting). Investment in current assets are also a part of investment decisions called as working capital decisions.

- Financial decisions - They relate to the raising of finance from various resources which will depend upon decision on type of source, period of financing, cost of financing and the returns thereby.

- Dividend decision - The finance manager has to take decision with regards to the net profit distribution. Net profits are generally divided into two:

- Dividend for shareholders- Dividend and the rate of it has to be decided.

- Retained profits- Amount of retained profits has to be finalized which will depend upon expansion and diversification plans of the enterprise.

6. What are the main objectives of financial management? Briefly explain

Ans:The financial management is generally concerned with procurement, allocation and control of financial resources of a concern. The objectives can be-

- To ensure regular and adequate supply of funds to the concern.

- To ensure adequate returns to the shareholders which will depend upon the earning capacity, market price of the share, expectations of the shareholders.

- To ensure optimum funds utilization. Once the funds are procured, they should be utilized in maximum possible way at least cost.

- To ensure safety on investment, i.e, funds should be invested in safe ventures so that adequate rate of return can be achieved.

- To plan a sound capital structure-There should be sound and fair composition of capital so that a balance is maintained between debt and equity capital.

7. How does working capital affect both the liquidity as well as profitability of a business?

Ans: Working capital of a business refers to the excess of current assets (such as cash in hand, debtors, stock, etc.) over current liabilities. Working capital affects both the liquidity as well as profitability of a business. As the amount of working capital increases, the liquidity of the business increases. However, since current assets offer low return, with the increase in working capital the profitability of the business falls. For example, an increase in the inventory of the business increases its liquidity but since the stock is kept idle, the profitability falls. On the other hand, low working capital, hinders the day to day operations of the business. Thus, the working capital should be such that a balance is maintained between the profitability and liquidity.

Long Answer Type:

1. What is working capital? How is it calculated? Discuss five important determinants of working capital requirement.

Ans: Every business needs to take the decision regarding the investment in current assets i.e. the working capital. Current assets refer to the assets that are converted into cash or cash equivalents in a short period of time (less than or equal to one year). There are two broad concepts of working capital namely, Gross working capital and Net working capital.

Gross working capital (or, simply working capital) refers to the investment done in the current assets. Net working capital, on the other hand, refers to the amount of current assets that is in excess of current liabilities. Herein, current liabilities are those obligatory payments which are due for payment such as bills payable, outstanding expenses, creditors, etc. Net Working Capital is calculated as the difference of current assets over current liabilities. i.e.

NWC = Current Assets - Current Liabilities

The following are five determinants of working capital requirement:

(i)Type of Business: Working capital requirement of a firm depends on its nature of business. An organisation that deals in services or trading will not require much of working capital. This is because such organisations involve small operating cycle and there is no processing done. Herein, the raw materials are the same as the outputs and the sales transaction takes place immediately. In contrast to this, a manufacturing firm involves large operating cycle and the raw materials need to be converted into finished goods before the final sale transaction takes place. Thereby, such firms require large working capital.

(ii)Scale of Operations: Another factor determining the working capital requirement is the scale of operations in which the firm deals. If a firm operates on a big scale, the requirement of the working capital increases. This is because such firms would need to maintain high stock of inventory and debtors. In contrast to this, if the scale of operation is small, the requirement of the working capital will be less.

(iii)Fluctuations in Business Cycle: Different phases of business cycle alter the working capital requirements by a firm. During boom period, the market flourishes and thereby, there is higher sale, higher production, higher stock and debtors. Thus, during this period the need for working capital increases. As against this, in a period of depression there is low demand, lesser production and sale, etc. Thus, the working capital requirement reduces.

(iv)Production Cycle: The time period between the conversion of raw materials into finished goods is referred as production cycle. The span of production cycle is different for different firms depending on which the requirement of working capital is determined. If a firm has a longer span of production cycle, i.e. if there is a long time gap between the receipt of raw materials and their conversion into final finished goods, then there will be a high requirement of working capital due to inventories and related expenses. On the other hand, if the production cycle is short then requirement of working capital will be low.

(v)Growth Prospects: Higher growth and expansion is related to higher production, more sales, more inputs, etc. Thus, companies with higher growth prospects require higher amount of working capital and vice versa.

2. ''Capital structure decision is essentially optimisation of risk-return relationship''. Comment.

Ans: Capital Structure refers to the combination of different financial sources used by a company for raising funds. The sources of raising funds can be classified on the basis of ownership into two categories as borrowed funds and owners' fund. Borrowed funds are in the form of loans, debentures, borrowings from banks, public deposits, etc. On the other hand, owners' funds are in the form of reserves, preference share capital, equity share capital, retained earnings, etc. Thus, capital structure refers to the combination of borrowed funds and owners' fund. For simplicity, all borrowed funds are referred as debt and all owners' funds are referred as equity. Thus, capital structure refers to the combination of debt and equity to be used by the company. The capital structure used by the company depends on the risks and returns of the various alternative sources.

Both debt and equity involve their respective risk and profitability considerations. While on one hand, debt is a cheaper source of finance but involves greater risk, on the other hand, although equity is comparatively expensive, they are relatively safe.

The cost of debt is less because it involves low risk for lenders as they earn an assured amount of return. Thereby, they require a low rate of return which lowers the costs to the firm. In addition to this, the interest on debt is deductible from the taxable income (i.e. interest that is to be paid to the debt security holders is deducted from the total income before paying the tax). Thus, higher return can be achieved through debt at a lower cost. In contrast, raising funds through equity is expensive as it involves certain floatation cost as well. Also, the dividends are paid to the shareholders out of after tax profits.

Though debt is cheaper, higher debt raises the financial risk. This is due to the fact that debt involves obligatory payments to the lenders. Any default in payment of the interest can lead to the liquidation of the firm. As against this, there is no such compulsion in case of dividend payment to shareholders. Thus, high debt is related to high risk.

Another factor that affects the choice of capital structure is the return offered by various sources. The return offered by each source determines the value of earning per share. A high use of debt increases the earning per share of a company (this situation is called Trading on Equity). This is because as debt increases the difference between Return on Investment and the cost of debt increases and so does the EPS. Thus, there is a high return on debt. However, even though higher debt leads to higher returns but it also increases the risk to the company.

Therefore, the decision regarding the capital structure should be taken very carefully, taking into consideration the return and risk involved.

3. ''A capital budgeting decision is capable of changing the financial fortunes of a business''. Do you agree? Why or why not?

Ans: Yes, capital budgeting decision is a very essential decision which needs to be taken carefully. It has the capability of changing the financial fortunes of a business. Capital budgeting decision refers to the decisions regarding the allocation of fixed capital to different projects. Such decisions involve investment decisions regarding attainment of new assets, expansion, modernisation and replacement. Such long term investments include purchasing plant and machinery, furniture, land, building, etc. and also expenditure as on launch of a new product, modernisation and advertising, etc. They have long term implications on the business and are irrevocable except at a huge cost. They affect a business' long term growth, profitability and risk.

The following are the factors that highlight the importance of capital budgeting decisions:

(i)Long Term Implications: Investment on capital assets (long term assets) yield return in the future. Thereby, they affect the future prospects of a company. A company's long term growth prospects depend on the capital budgeting decisions taken by it.

(ii)Huge Amount of Funds: Investing in fixed capital involves a large amount of funds. This makes the capital budgeting decisions all the more important as huge amount of funds remain blocked for a longer period of time. These decisions once made are difficult to change. Thus, capital budgeting decisions need to be taken carefully after a detailed study of the total requirement of funds and the sources from which they are to be raised.

(iii)High Risk: Fixed assets involve huge amount of money and thereby, involve huge risk as well. Such decisions are risky as they have an impact on the long term existence of the company. For example, decision about the purchase of new machinery involves a risk in terms of whether the return from the machinery would be greater than the cost incurred on it.

(iv)Irreversible Decisions: These decisions once made are irrevocable. Reversing a capital budgeting decision involves huge cost. This is because once huge investment is made on a project, withdrawing it would mean huge losses.

4. Explain the factors affecting the dividend decision.

Ans: Dividend decision of a company deals with what portion of the profits is to be distributed as dividends between the shareholders and what portion is to be kept as retained earnings. The following are the factors that affect the dividend decision.

1. Legal requirements

There is no legal compulsion on the part of a company to distribute dividend. However, there certain conditions imposed by law regarding the way dividend is distributed. Basically there are three rules relating to dividend payments. They are the net profit rule, the capital impairment rule and insolvency rule.

2. Firm's liquidity position

Dividend payout is also affected by firm's liquidity position. In spite of sufficient retained earnings, the firm may not be able to pay cash dividend if the earnings are not held in cash.

3. Repayment need

A firm uses several forms of debt financing to meet its investment needs. These debt must be repaid at the maturity. If the firm has to retain its profits for the purpose of repaying debt, the dividend payment capacity reduces.

4. Expected rate of return

If a firm has relatively higher expected rate of return on the new investment, the firm prefers to retain the earnings for reinvestment rather than distributing cash dividend.

5. Stability of earning

If a firm has relatively stable earnings, it is more likely to pay relatively larger dividend than a firm with relatively fluctuating earnings.

6. Desire of control

When the needs for additional financing arise, the management of the firm may not prefer to issue additional common stock because of the fear of dilution in control on management. Therefore, a firm prefers to retain more earnings to satisfy additional financing need which reduces dividend payment capacity.

7. Access to the capital market

If a firm has easy access to capital markets in raising additional financing, it does not require more retained earnings. So a firm's dividend payment capacity becomes high.

8. Shareholder's individual tax situation

For a closely held company, stockholders prefer relatively lower cash dividend because of higher tax to be paid on dividend income. The stockholders in higher personal tax bracket prefer capital gain rather than dividend gains.

5. Explain the term ''Trading on Equity''. Why, when and how it can be used by a company?

Ans: Trading on equity refers to a practice of raising the proportion of debt in the capital structure such that the earnings per share increases. A company resorts to Trading on Equity when the rate of return on investment is greater than the rate of interest on the borrowed fund. That is, the company resorts to Trading on Equity in situation of favourable financial leverage. As the difference between the return on investment and the rate of interest on debt increases, the earnings per share increase.

The use of Trading on Equity is explained in detail with the help of the following example.

Suppose there are two situations for a company. In situation I it raises a fund of Rs 5,00,000 through equity capital and in situation II, it raises the same amount through two sources- Rs 2,00,000 through equity capital and the remaining Rs3,00,000 through borrowings.

Also suppose the tax rate is 30% and the interest on borrowings is 10%. The earnings per share (EPS) in the two situations is calculated as follows.

Situation I | Situation II | |

Earnings before interest and tax (EBIT) | 1,00,000 | 1,00,000 |

Interest | 30,000 | |

Earnings Before Tax (EBT) | 1,00,000 | 70,000 |

Tax | 30,000 | 21,000 |

Earnings After Tax (EAT) | 70,000 | 79,000 |

No. Of equity shares | 50,000 | 20,000 |

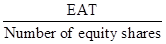

EPS= |

|

|

=1.4

=1.4 =3.95

=3.95Clearly, in the second situation the EPS is greater than in the first situation. In the second situation the company takes advantage of the Trading on Equity and raises the EPS. Here, the return on investment calculated as  is 20% while the interest on the borrowings is 10%. Thus, the Trading on Equity is profitable.

is 20% while the interest on the borrowings is 10%. Thus, the Trading on Equity is profitable.

However, it should be noted that Trading on Equity is profitable and should be used only when the return on investment is greater than the interest on borrowed funds. In case the return on investment is less than the rate of interest to be paid, the Trading on Equity should be avoided.

Suppose instead of Rs 1,00,000 the company earns just Rs 25,000. In such a case the EPS are calculated as follows.

Situation I | Situation II | |

Earnings before interest and tax (EBIT) | 40,000 | 40,000 |

Interest | 10,000 | |

Earnings Before Tax (EBT) | 25,000 | 10,000 |

Tax | 30,000 | 3,000 |

Earnings After Tax (EAT) | 70,000 | 7,000 |

No. Of equity shares | 50,000 | 20,000 |

EPS= |

|

|

=3.5

=3.5Clearly in this case, the EPS in Situation II falls. Here the return on investment is only 8% while the interest on the borrowings is 10%.

while the interest on the borrowings is 10%.

Thus, in this situation the Trading on Equity is not favourable and should be discouraged. Hence, it can be said that a firm can use Trading on Equity if it is earning high profits and can increase the EPS by raising more funds through borrowings.