Financial Management - Revision Notes

CBSE Class 12 Business Studies

Revision Notes

CHAPTER – 9

FINANCIAL MANAGEMENT

Introduction

• Business Finance = Money or funds available for a business for its operations (that is, for some specific purpose) is called finance. It is indispensable for survival and growth of business, for production and distribution of goods and meeting day to day expenses etc.

• It involves acquiring funds to buy Fixed assets (tangible and intangible) and Raw materials and maintain working capital.

Financial Management includes those business activities that are concerned with acquisition and conservation of capital funds in meeting the financial needs and overall objectives of a business enterprise.

Aims of Financial Management:

- Reduce cost of funds procured

- Keep risks under control

- Achieve effective employment of fund

- Ensure availability of sufficient funds while avoiding idle funds

•bjectives of Financial Management

• Primary objective: To maximize wealth of owners in the long run – Wealth Maximization concept.

• ‘Owners’ of a company are the shareholders.

• The term wealth refers to wealth of owners as reflected by the market price of their shares.

• The market price of shares is linked to three basic financial decisions:

• Investment decision • Financing decision and • Dividend decision

• Market price of a share will increase if benefits from a decision are greater than the cost involved in it.

• The goal of a firm should be to maximize the wealth of owners in the long run.

• Increase in the market price of shares is an indicator of the financial health of a firm.

• Other objectives that help a firm achieve the primary objective are:

Ensure availability of funds at reasonable costs:

Ensure effective utilization of funds:

Ensure safety of funds thro creation of reserves:

Maintain liquidity and solvency:

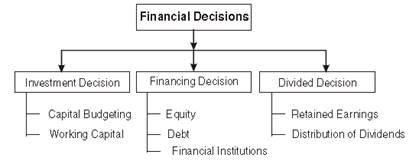

Financial Decisions

Every company is required to take three main financial decisions which are as follows:

1. Investment Decision

Resources are scarce and can be put to alternate use. A firm must choose where to invest so as to earn the highest possible profits.

Investment decision relates to decisions about how the firm‘s funds are invested in different assets that is, different investment proposals

Has two components:

• Working Capital Decisions - Short Term investment decisions.

• Capital Budgeting decisions – Long Term investment decisions

Factors affecting Investment Decisions/Capital Budgeting decisions

1. Cash flows of the project: The series of cash receipts and payments over the life of an investment proposal should be considered and analyzed for selecting the best proposal.

2. Rate of Return: The expected returns from each proposal and risk involved in them should be taken into account to select the best proposal.

3. Investment Criteria Involved: The various investment proposals are evaluated on the basis of capital budgeting techniques. These involve calculation regarding investment amount, interest rate, cash flows, rate of return etc.

2. Financing Decision

• These are decisions w.r.t quantum of finance or composition of funds from various longterm sources.(short term = working capital management)

• Financing decisions involve: a) Decision whether or not to use a combination of ownership and borrowed funds. b) Determining their precise ratio.

• Firm needs a judicious mix of debt and equity as :

• Debt involves ‘Financial Risk‘ = risk of default on payment of interest on borrowed funds and the repayment of the principle amount whereas

• Shareholders‘ funds involve no fixed commitment w.r.t payment of returns or repayment of capital.

• Ownership fund vs. Debt fund: They can be compared on the basis of factors such as examples, interest/dividend payout and repayment of principle, tax deductibility, and risk and floatation costs.

Factors Affecting Financing Decision

1. Cost: The cost of raising funds from different sources are different. The cheapest source should be selected.

2. Risk: The risk associated with different sources is different. More risk is associated with borrowed funds as compared to owner’s fund as interest is paid on it and it is repaid also, after a fixed period of time or on expiry of its; tenure.

3. Flotation Cost: The costs involved in issuing securities such as brokers commission, underwriters’ fees, expenses on prospectus etc. are called flotation costs. Higher the flotation cost, less attractive is the source of finance.

4. Cash flow position of the business: In case the cash flow position of a company is good enough then it can easily use borrowed funds and pay interest on time.

5. Control Considerations: In case the existing shareholders want to retain the complete control of business then finance can be raised through borrowed funds but when they are ready for dilution of control over business, equity can be used for raising finance.

6. State of Capital Markets: During boom, finance can easily be raised by issuing shares but during depression period, raising finance by means of debt is easy.

7. Period of Finance: For permanent capital requirement, Equity shares must be issued as they are not to be paid back and for long and medium term requirement, preference shares or debentures can be issued.

3. Dividend Decision

• Dividend is that portion of divisible profits that is distributed to the owners i.e. the shareholders. It results in current income for the shareholders.

• Retained earnings= proportion of profits kept in, that is, reinvested in the business for the business.

• Dividend decision= whether to distribute earnings to shareholder as dividends or retain earnings to finance long-term profits of the firm. Must be done keeping in mind the firms overall objective of maximizing the shareholders wealth.

Factors affecting Dividend Decision

1. Earnings: Companies having high and stable earning could declare high rate of dividends as dividends are paid out of current and paste earnings.

2. Stability of Dividends: Companies generally follow the policy of stable dividend. The dividend per share is not altered and changed in case earnings change by small proportion or increase in earnings is temporary in nature.

3. Growth Prospects: In case there are growth prospects for the company in the near future them it will retain its earning and thus, no or less dividend will be declared.

4. Cash Flow Positions: Dividends involve an outflow of cash and thus, availability of adequate cash is for most requirement for declaration of dividends.

5. Preference of Shareholders: While deciding about dividend the preference of shareholders is also taken into account. In case shareholders desire for dividend then company may go for declaring the same.

6. Taxation Policy: A company is required to pay tax on dividend declared by it. If tax on dividend is higher, company will prefer to pay less by way of dividends whereas if tax rates are lower then more dividends can be declared by the company.

7. Issue of bonus shares: Companies with large reserves may also distribute bonus shares to increase their capital base as it signifies growth of the company and enhances its reputation also.

8. Legal constraints: Under provisions of Companies Act, all earnings can’t be distributed and the company has to provide for various reserves. This limits the capacity of company to declare dividend.

Financial Planning

• It involves preparation of a financial blueprint of an organization. It is the process of estimating the fund requirement of a business and determining the possible sources from which it can be raised.

• Objectives of Financial Planning:

• To ensure availability of funds whenever they are required o Includes estimation of the funds required for different purposes (long term assets/working cap requirement)

• Estimate the time at which these funds need to be made available.

• Specify sources of these funds.

• To see that the firm does not raise resources unnecessarily:

• Shortage of funds => firm cannot meet its payment obligations.

• Surplus funds => do not earn returns but adds to costs.

Importance of Financial Planning

1. To ensure availability of adequate funds at right time.

2. To see that the firm does not raise funds unnecessarily.

3. It provides policies and procedures for the sound administration of finance function.

4. It results in preparation of plans for future. Thus new projects can he under taken smoothly.

5. It attempts to achieve a balance between inflow and outflow of funds. Adequate liquidity is ensured throughout the year.

6. It serves as the basis of financial control. The management attempts to ensure utilization of funds in tune with the financial plans.

Capital Structure

• On the basis of ownership, funds => owners funds + borrowed funds.

• Owners funds = equity share capital + preference share capital + reserves and surpluses + retained earnings = EQUITY

• Borrowed funds = loans + debentures + public deposits = DEBT

• Capital Structure = The mix of long-term sources of funds

• Refers to the proportion of debt and equity used for financing the operations of a business.

• Cost and risk- Debt Vs Equity:

• Cost of Debt is lower than cost of equity but Debt is more risky than equity.

• Cost of debt < cost of equity as lenders risk < owners risk.

• Lender earns an assured interest and repayment of capital..

• Interest on debt is a tax deductible expense so brings down the tax liability for a business whereas dividends are paid out of profit after tax.

• Debt is more risky for the business as it adds to the financial risk faced by a business.

• Any default w.r.t payment of interest or repayment of principle amt may lead to liquidation.

• Capital structure affects both the profitability and the financial risk faced by a business.

• Optimal Capital Structure is that combination of debt and equity that maximizes the market value of shares of that company

Factors Affecting Capital Structure

i. Cash flow position:

a. The size of the projected cash flows must be considered before deciding the capital structure of the firm. If there is sufficient cash flow, debt cab be used.

b. It must cover fixed payment obligations w r t:

i. Normal business operations ii. Investment in fixed assets iii. Meeting debt service commitments as well as provide a sufficient buffer.

ii. Interest coverage ratio :

a. Higher the Interest coverage ratio which is calculated as follows: EBIT/ Interest, lower shall be the risk of the company failing to meet its interest payment obligations.

b. Low Interest coverage ratio => debt ≠ used.

iii. Debt Service Coverage Ratio:

a. Debt service coverage ratio = Profit after tax + Depreciation + Interest + Non Cash exp. Pref. Div + Interest + Repayment obligation

b. A higher Debt service coverage ratio, in which the cash profits generated by the operations are compared with the total cash required for the service of debt and the preference share capital, the better will the ability of the firm to increase debt component in the capital structure.

c. Low Debt service coverage ratio => debt ≠ used.

iv. Return On Investment

a. If return on investment of the company is higher, the company can choose to use trading on equity to increase its EPS, i.e., its ability to use debt is greater.

v. Cost Of Debt

a. More debt can be used if cost of Debt is low.

vi. Tax Rate

a. A higher tax rate makes debt relatively cheaper and increases its attraction as compared to equity.

vii. Cost Of Equity

a. when the company uses more debt, the financial risk faced by equity holders increase so their desired rate of return increases.

b. If debt is used beyond a point, cost of equity may go up sharply and share price may decrease in spite of increased EPS.

viii. Floatation Cost

a. Cost of Public issue is more than the floatation cost of taking a loan.

b. The floatation cost may affect the choice between debt and equity and hence the capital structure

ix. Risk Consideration:

a. The total risk of business depends upon both the business risk and financial risk. If a firm‘s business risk is lower, its capacity to use debt is higher and vice versa.

x. Flexibility:

a. If the firm uses its debt potential, it loses the flexibility to use more debt.

b. To maintain flexibility the company must maintain some borrowing power to take care of unforeseen circumstances.

xi. Control:

a. Debt normally does not cause dilution of control whereas a public issue makes the firm vulnerable to takeovers.

b. To retain control, firm should issue debt.

Fixed Capital

Fixed capital refers to investment in long-term assets. Investment in fixed assets is for longer duration and they must be financed through long-term sources of capital. Decisions relating to fixed capital involve huge capital funds and are not reversible without incurring heavy losses.

Factors Affecting Requirement of Fixed Capital

1. Nature of Business: Manufacturing concerns require huge investment in fixed assets & thus huge fixed capital is required for them but trading concerns need less fixed capital as they are not required to purchase plant and machinery etc.

2. Scale of Operations: An organization operating on large scale requires more fixed capital as compared to an organization operating on small scale.

For Example - A large scale steel enterprise like TISCO requires large investment as compared to a mini steel plant.

3. Choice of Technique: An organization using capital intensive techniques requires more investment in plant & machinery as compared to an organization using labour intensive techniques.

4. Technology upgradation: Organizations using assets which become obsolete faster require more fixed capital as compared to other organizations.

5. Growth Prospects: Companies having more growth plans require more fixed capital. In order to expand production capacity more plant & machinery are required.

6. Diversification: In case a company goes for diversification then it will require more fixed capital to invest in fixed assets like plant and machinery.

7. Distribution Channels: The firm which sells its product through wholesalers and retailers requires less fixed capital.

8. Collaboration: If companies are under collaboration, Joint venture, then they need less fixed capital as they share plant & machinery with their collaborators.

Working Capital

Working Capital refers to the capital required for day to day working of an organization. Apart from the investment in fixed assets every business organization needs to invest in current assets, which can be converted into cash or cash equivalents within a period of one year. They provide liquidity to the business. Working capital is of two types - Gross working capital and Net working capital. Investment in all the current assets is called Gross Working Capital whereas the excess of current assets over current liabilities is called Net Working Capital. Following are the factors which affect working capital requirements of an organization:

l. Nature of Business: A trading organization needs a lower amount of working capital as compared to a manufacturing organization, as trading organization undertakes no processing work.

2. Scale of Operations: An organization operating on large scale will require more inventory and thus, its working capital requirement will be more as compared to small organization.

3. Business Cycle: In the time of boom more production will be undertaken and so more working capital will be required during that time as compared to depression.

4. Seasonal Factors: During peak season demand of a product will be high and thus high working capital will be required as compared to lean season.

5. Credit Allowed: If credit is allowed by a concern to its customers than it will require more working capital but if goods are sold on cash basis than less working capital is required.

6. Credit Availed: If a firm is able to purchase raw materials on credit from its suppliers than less working capital will be required.

7. Inflation: Working capital requirement is also determined by price level changes. For example, during inflation prices of raw material, wages also rise resulting in increase in working capital requirements.

8. Operating Cycle/Turnover of Working Capital: Turnover means speed with which the working capital is converted into cash by sale of goods. If it is speedier, the amount of working capital required will be less.