Introduction to Microeconomics & Central Problems - Test Papers

CBSE Test Paper-01

Class – 11 Economics (Economy and central problems of an Economy)

General Instruction:

- All questions are compulsory.

- Marks are given alongwith their questions.

- Socialist economy is a (1)

- Planned economy

- Mixed economy

- Profit oriented economy

- None of these

- Consider the following and decide which, if any, economy is without scarcity (1)

- The pre-independent Indian economy, where most people were farmers

- A mythical economy where everybody is a billionaire

- Any economy where income is distributed equally among its people

- None of these

- ‘Opportunity cost is not an actual cost’. Do you agree? (2)

- If production possibility curve shifts to the right, should it be parallel to the old one? (2)

- Why is production possibility curve called opportunity cost curve? (3)

- Explain how scarcity and choice go together. (3)

- State reasons why an economic problem arises. (4)

- How is ‘choice’ a core parameter in the study of economics? (4)

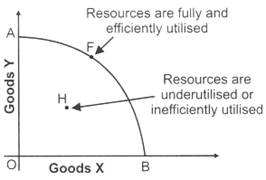

- “An economy always produces on but not inside a PPC.” Defend or refute. (6)

- What is Marginal Rate of Transformation? Explain with the help of an example. (6)

CBSE Test Paper-01

Class – 11 Economics (Economy and central problems of an Economy)

Answers

- a) Planned economy

- d) None of these

- Opportunity cost is not an actual cost; in fact, it is the cost of next best alternative available but not actually opted for in the decision-making process.

- The slope of production possibility curve indicates Marginal Opportunity cost, which may be different at different levels of output. So, if PPC shifts to the right, it will not be parallel to the old one.

- Production possibility curve is called opportunity cost curve because the slope of the curve at each and every point measures the opportunity cost of one commodity in terms of an alternative commodity given up. The rate of this sacrifice is called the marginal opportunity cost.

- Resources are not only scarce but also have alternative uses. For example, Land which can be used for various purposes. Hence, the problem of choice is the essence of an economic problem. However, if resources were not scarce, one could have everything at any time and there would be no problem of choice.

- Following are the reasons for an economic problem to arise:

- Resources are scarce.

- Resources have alternative uses.

- Wants are unlimited.

- Wants are recurring in nature.

- Economics deal with the human behaviour in the face of wants and resources to satisfy these wants. Now, a unique feature of human behaviour is unlimited wants. In comparison to this, the resources to satisfy these wants are limited. And these resources have alternative uses. But, if the resources are allocated to the production of one good, then the economy will have to forgo the production of another good. In this way, the economy has to trade off between the production of selected goods. Therefore, in order to allocate these resources in the best possible manner, there arises the problem of choice. This problem of choice (due to the scarcity of resources) becomes the core parameter in the study of economics as it gives rise to the central problems of an economy.

- The given statement is refuted. An economy operates on PPC, only when resources are fully and efficiently utilised. It means, if there is unemployment or inefficient use of resources, the economy may operate inside PPC. So, the economy may operate at point ‘H’ (Figure), in addition to the points on the curve AB on PPC. What is not possible for a country to produce outside the PPC, as these points are not feasible; they are beyond a country’s capacity.

- The marginal rate of transformation is the rate at which one good must be sacrificed in order to produce a single extra unit (or marginal unit) of another good, assuming that both goods require the same scarce inputs. The marginal rate of transformation is tied to the production possibilities frontier (PPF), which displays the output potential for two goods using the same resources. To produce more of one good means producing less of the other because the resources are efficiently allocated.

The marginal rate of transformation is the absolute value of the slope of the production possibilities frontier. For each point on the frontier (which is displayed as a curved line), there is a different marginal rate of substitution, based on the economics of producing each product individually.

Marginal rate of transformation (MRT)

∆y = Change in production of y

∆x = Change in production of xProduction of x Production of y MRT 0 10000 - 1 9000 10000:1 2 7500 1500:1 3 5500 2000:1