Cash Book - Revision Notes

CBSE Class 11 Accountancy

Revision Notes

Chapter 4 Recording of Transactions -II Cash Books and other Books

Books of Original Entry/Special Purpose Books

As the business grows and number of transactions increase, it becomes necessary for the necessary for the business to divide the recording work. The books maintained are illustrated below:

| Transactions | Further classification | Subsidiary Books Maintained |

| Cash & Bank Related Transactions | Only Cash | Simple Cash Book |

| Cash & Bank Transactions | Double Column Cash book | |

| Cash payment of small amount | Petty Cash Book | |

| Transaction Other than Cash & Bank | Credit Sale | Sales Book |

| Credit Purchases | Purchases Book | |

| Sales Returns/ Returns Inward | Sales returns Book | |

| Purchases Returns /Returns outward | Purchases Returns Book | |

| Any other transaction | Journal Proper |

Advantages of Maintaining Subsidiary Books

- Division of work

- Leads to Specialization

- Easy to maintain Ledger

- Check on frauds

- Easy to fix responsibility

- Quick availability of required information.

Cash Book

Cash book shows all the transactions related to cash receipts and payments. Cash book serves two purposes. First, all the cash transactions are recorded first time in cash book it becomes Book of original entry. Second, there is no need to prepare Cash a/c in ledger it also play the role of Principal Book.

Simple Cash Book

All the cash receipts are shown in left hand side i.e. Debit side and all the cash payments are shown in right hand side i.e. Credit Side.

Points to Remember

- Cash in hand/opening balance of cash is shown in Dr. side of the Cash book as “To Balance b/d”

- Only transactions of cash receipts and payments are recorded in this book.

- This book never shows a credit balance because one can’t pay more than the cash one have.

Cash Book with Cash and Bank Column

In this case the Cash Book is ruled with two amount columns on either side of the cash book namely, "Cash and Bank". Cash columns in such a case will record actual cash received in the debit side and payments in the credit side. Cheques received should be entered on the debit side of the bank column when it deposited in the bank. The payments by cheques should be entered on the credit side in bank column and also when cash is withdrawn from the bank.

Important Entries

1. Contra Entries : These entries affect cash and bank columns both at the same time. To indicate contra entry “C” is mentioned in the L.F. column of the cash Book. Following two cases result in Contra entries.

(a) Depositing cash into Bank Rs. 1,000 It will increase bank balance, so bank column is debited and flash balance will decrease, so cash column is credited.

| Dr. | Cash Book (with Cash & Bank Column) | Cr. | |||||||||||

| Date | Particulars | V.N. | L.F. | Cash Rs. | Bank Rs. | Disc ount | Date | Particulars | V.N. | L.F. | Cash Rs. | Bank Rs. | Disc ount |

| 2015 Apr 01 | To Cash A/c | 1,000 | 2015 | By Bank A/c | C | 1,000 | |||||||

(b) Withdrawn from Bank for office use Rs. 1,000. It will increase cash balance, so cash column is debited and bank balance will decrease, so bank column is credited.

| Dr. | Cash Book (with Cash & Bank Column) | Cr. | |||||||||||

| Date | Particulars | V.N. | L.F. | Cash Rs. | Bank Rs. | Disc ount | Date | Particulars | V.N. | L.F. | Cash Rs. | Bank Rs. | Disc ount |

| 2015 Apr 01 | To Bank A/c | C | 1,000 | 2015 | By Cash A/c | C | 1,000 | ||||||

(2) Entries relating to cheques :

- When any payment is made by cheque : It will reduce the bank balance and thus bank column will be credited.

- When any payment is received in the form of cheque and no information about its deposit into bank is given. In this case it is assumed that the cheque is deposited into bank on the same day, when it is received & so bank A/c will be debited.

- When any payment is received in the form of cheque and it is deposited into bank on same day than bank A/c will be debited.

When payment is receive in the form of cheque on one day & its is deposited into Bank on other day i.e. when two dates, one for the receipt of cheque and the other for deposit. In this case no entry it to be recorded at the time of receiving the cheque. Entry is to made when cheque deposited in the bank, as bank column is debited.

Petty Cash Book

Business has to incur small expenses which are repetitive in nature. To save the time and efforts of head cashier, business appoints a petty cashier. He is entrusted with the duty of paying these expenses.

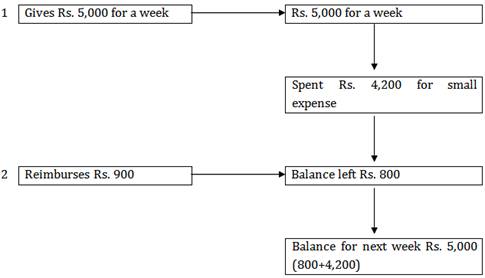

Imprest System of Petty Cash Book

Under this system, Head cashier gives a fixed amount to petty cashier for a definite period. At the end of given period, Head cashier reimburses the amount actually spent by the petty cashier resulting the same amount with petty cashier which he had in the beginning of the period.

This can be illustrated as under.

Head Cashier Petty Cashier

Advantage of Petty Cash Book

- Saving of time and efforts of Head cashier

- Control on Petty expenses.

- Less chances of fraud.

Special Purpose Subsidiary Books

Purchases Book

In this book, only those transactions are recorded which are related to credit purchases of goods in which the business deals in. Recording is made on the basis of Bills/ Invoices issued by the Suppliers.

Transactions not recorded in purchases Book

- Purchases of goods for cash.

- Purchases of Assets meant for long term, not for resale.

Sales Books/Sales Journal

In this book, transactions for credit sales of goods are recorded. The source documents for this book is duplicate copy of invoice/bills issued to the customers.

Transactions not recorded in Sales Book

- Sales of goods for cash

- Sales of Assets.

Purchases Returns/Returns Outward Book

This book includes only those transactions which are related to returns of goods bought on credit. The goods may be returned due to various reasons such as goods bought being defective, supply of inferior quality goods etc. Entries in this book are made on the basis of Debit Note. A Debit note contains the name of the supplier to whom good are returned, details of goods returned

Sales Returns Book

This book includes all the returns by customers of credit sales of goods. The Credit Note is used for recording entries in this book. The credit note contains the details of customers and goods returned.